One of the great tax advantages of a Self-Invested Personal Pension is that it allows you to pass on your pension to your beneficiaries on your death. Your beneficiaries can normally choose to take the pension fund as a lump sum or leave it invested in a SIPP.

What happens to my SIPP upon death?

You can nominate whoever you like to receive your SIPP on your death. This could be your spouse, children or grandchildren, or you can nominate someone unrelated to you if you wish. You can also leave some, or all, of your SIPP to charity.

You don’t need to leave your pension to just one person; you can split it in whatever proportion you like, so each of your beneficiaries receives a share.

Are my nominations binding?

As the scheme administrator of your SIPP, AJ Bell has discretion over how your pension is passed on. However, it's rare that nominations aren't followed. Usually, this only happens if there's been a change of circumstances (for instance, a divorce), and your wishes haven't been updated.

How are death benefits paid?

Beneficiaries of your pension will normally have the choice of taking the pension fund as a lump sum or leaving the fund invested and using it to provide an income.

If they choose to leave the pension fund invested, they can take income as and when required. Any funds left invested will continue to benefit from being in a tax-advantaged pension wrapper.

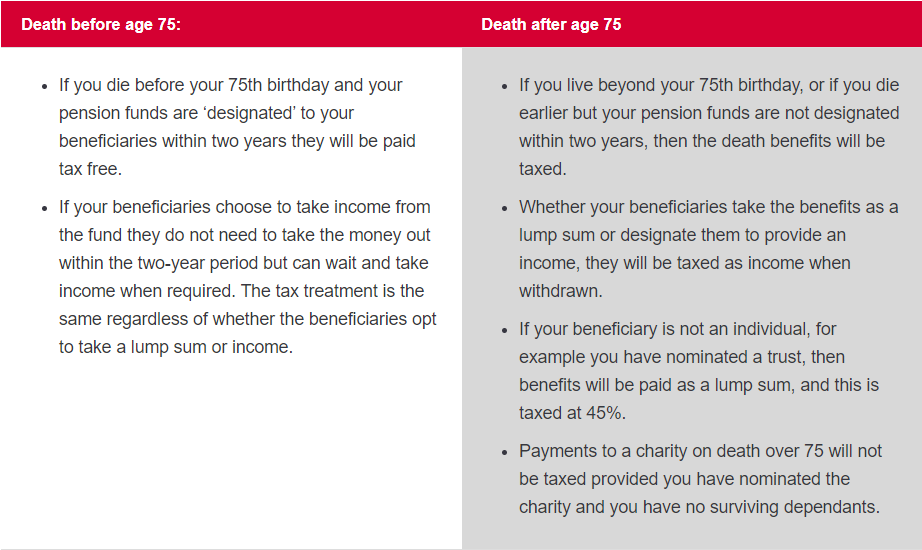

What tax will need to be paid?

The tax treatment of death benefits paid from your pension depends on two factors:

- Your age when you die.

- Whether or not the pension funds are ‘designated’ to your beneficiary within two years. ‘Designating’ the funds just means transferring them into the beneficiaries’ names.

What happens to the SIPP when the beneficiary dies?

If your beneficiary has not withdrawn the entire pension fund before their death, then the funds can be passed on again. Your beneficiary will be able to nominate successors who they want the funds to go to following their death.

The successors will then have the option of taking the funds as a lump sum or using it to provide an income. The tax treatment of the death benefits will depend on the age of the beneficiary who was holding the pension at their death, not on how old you were at your death.

As an example, if you live to be 90 and leave the fund to your child aged 60, then the death benefits payable to your child would be taxed (as you lived to be over 75). If your child took the benefits as income and the fund had not all been used before their death at age 70, then the remaining fund could be passed on to their successors tax free as they died before age 75.

It is possible to have unlimited successors, so your pension fund could be passed on for generations if it is not all taken out.

Case study: Graham Smith dies at aged 80 with £500,000 invested in a SIPP.

He has the following family:

Graham Smith wanted to ensure that on his death his wife had sufficient resources to live on. As his pension fund was substantial he did not believe she would need the entire SIPP and wanted to pass his SIPP on in a tax-efficient manner. He therefore completed an expression of wish leaving 60% of his pension fund to his wife, and 10% to each of his grandchildren.

- Caroline Smith, wife, 72, basic rate taxpayer

- Lucy, daughter, 50, higher rate taxpayer

- Sam, son, 47, higher rate taxpayer

- Adam, grandson, 20, non taxpayer

- Bella, granddaughter, 18, non taxpayer

- Charlie, grandson, 12, non taxpayer

- Darcy, granddaughter, 9, non taxpayer

Graham was over 75 when he died so any benefits paid out are taxable at the recipient’s marginal rate. Caroline Smith will pay basic rate tax at 20% (provided she doesn’t take income that takes her above the threshold for higher rate tax). Each grandchild can take up to £12,570 out each year without paying any tax (as they are non-taxpayers with no other income). They do not need to take any income if they do not want to.

If they did become higher rate tax payers in the future they could opt to leave the money in a pension even until their own retirement when their tax rate may drop.

Unfortunately Caroline Smith only lives for another two years. She has nominated her two children, Lucy and Sam, to be the beneficiaries of her fund on a 50/50 basis. As Caroline is only 74 at the time of her death, Lucy and Sam can take the benefits out free of income tax, despite the fact the funds originated from Graham Smith.

Our team are on hand to support you with any query that you may have, so feel free to get in touch.