A SIPP offers two main tax benefits. First, your investments will grow free from capital gains and income tax. Second, and more importantly, when paying into your SIPP, you receive government tax relief. How much depends on your circumstances – bearing in mind that pension and tax rules could change.

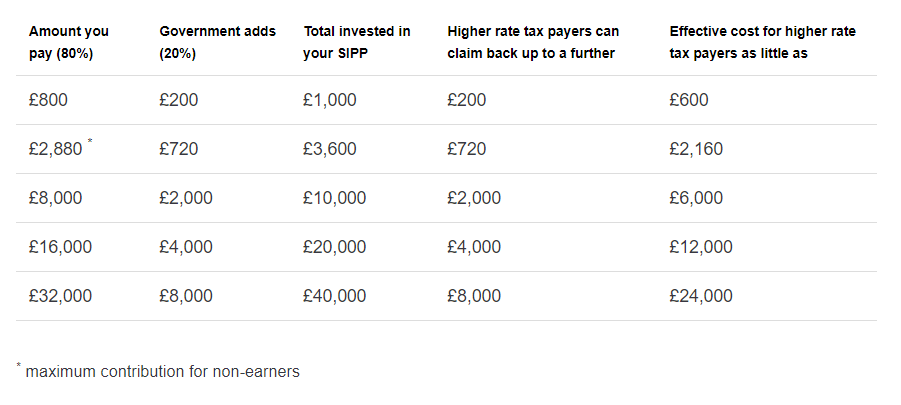

Any personal contributions you make, up to the amount you earn, are given basic rate tax relief at 20%. So if you pay £800 into your SIPP, the taxman will put in another £200 to make it up to £1,000. Those with no UK earnings at all can make contributions up to £3,600 a year including tax relief, so you would put in £2,880 and HM Revenue & Customs (HMRC) would add a further £720 directly into the SIPP.

If you are a higher rate taxpayer, you can claim extra tax relief through your self-assessment. This is sent to you directly from HMRC.

The benefits soon add up. A higher rate taxpayer putting £8,000 into their pension would get £2,000 added to their pot, and receive up to £2,000 as a rebate directly from HMRC, so the total cost to the higher rate taxpayer is £6,000 for a SIPP worth £10,000.

While you have the benefit of this generous tax relief, you must realise that you cannot access the money until you are at least 55 (57 from 6 April 2028).

The table below shows the tax benefits of investing in a SIPP:

You can contribute the equivalent of 100% of your earnings up to a maximum of £60,000 – the annual allowance for 2023/24. Employer contributions are included in the £60,000 limit and you are able to ‘carry forward’ unused allowances from up to three previous tax years.

This annual allowance is tapered for high income individuals. In the 2023/24 tax year, for every £2 of adjusted income over £260,000, the annual allowance is reduced by £1. The maximum reduction is £50,000, meaning that someone with adjusted income of over £360,000 has an annual allowance of £10,000.

Download annual allowance tapering guide

If you own your business, you can pay part of your salary directly into your pension as a company contribution. Employer pension contributions no longer count as profit – meaning your business is liable for less corporation tax – and a lower salary means less income tax for you to pay. Read more about pensions for the self-employed.

If you’ve flexibly accessed your pension, the amount you can pay into money purchase schemes, including your SIPP, each year is reduced from £60,000 to £10,000. You also lose the option of ‘carrying forward’ unused allowances in your SIPP.

The maximum that you can save tax free in pension savings is £1,073,100 – this is called the ‘lifetime allowance’ and is calculated across all pensions except the state pension. The money invested in your SIPP grows free of capital gains tax and income tax.

This information is based on the legislation as it stands now, but as with anything pension-, investment- or tax-related the rules can change in the future. Remember too that you will see your investment values fall as well as rise. You need to be prepared for this because your money is locked into your SIPP until you are at least 55 (57 from 6 April 2028), so you will not be able to access it.

For more information please read the key features and terms and conditions of our SIPP. Otherwise, you can contact our team who are on hand to help with any queries.